A Look into the Markets

This week, the Federal Reserve raised the Fed Funds Rate by .50%, the smallest hike in over 6 months, and in response, home loan rates improved. Let’s discuss the seemingly odd market reaction and what to watch in the week ahead.

“Slow ride, take it Easy” – Slow Ride by Foghat

“We’ve covered a lot of ground, full effects of tightening yet to be felt” – Fed Chair Jerome Powell – 12/14/22

This line from the Fed Chair’s press conference highlights the Fed’s action of smaller rate hikes as we approach what is the “terminal rate” or peak in the Fed Funds Rate.

The Fed Chair also reiterated that while the Fed is doing a smaller hike it is going to take time for the previous hikes to tamp down inflation pressures and elevate unemployment. And they will stay the course until the job is done.

Fed’s Summary of Economic Projections

Every three months, the Fed revises its outlook on economic growth, inflation, unemployment, and the Fed Funds Rate. What does the Fed think about 2023, and what has changed since September?

The Fed now sees the economy growing by just .50% in 2023, well below the 1.2%, they forecasted 90 days ago.

On inflation, the Fed expects their favored measure, The Core PCE, to come in at 3.5%, above their previous estimate of 3.1%.

Unemployment is expected to be 4.6%, higher than the 4.4% they previously expected.

3.46%

It’s a good time to remember that the Fed controls the Fed Funds Rate, which is an overnight lending rate, and their hiking activity has no direct correlation to home loan rates.

Long-term Treasury rates, like the 10-yr Note, move higher if the economy can absorb the Fed rate hikes. Seeing the 10-yr Note yield at 3.46% after the Fed raised the Fed Funds Rate to 4.50% tells us the bond market feels the slowing economic conditions are not supportive of higher rates and the Fed will have to change course at some point.

Bottom line: Home loan rates are at the best levels since September. Couple this with sellers eager to make deals and you have the recipe for an opportunity for nimble buyers.

Looking Ahead

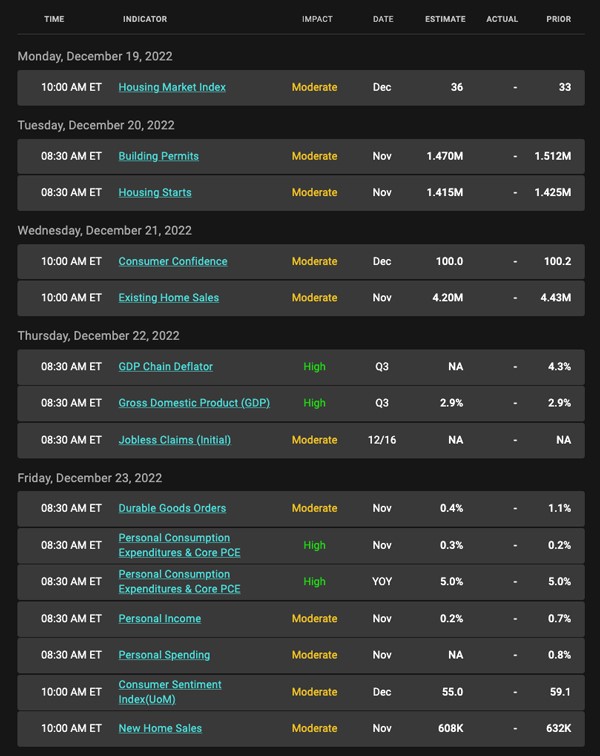

Back to the data. Next week brings the Fed’s favored gauge of consumer inflation, the Core PCE. We will also have readings on GDP, Consumer Sentiment, and housing.

Mortgage Market Guide Candlestick Chart

Mortgage-backed security (MBS) prices determine home loan rates. The chart below is a one-year view of the Fannie Mae 30-year 5.5% coupon, where currently closed loans are being packaged. As prices go higher, rates move lower, and vice versa.

You can see on the right side of the chart the Green Candles moving above $101 after the Fed raised rates. With the 10-yr beneath 3.50%, it may help put a near-term cap on how high mortgage rates go.

Chart: Fannie Mae Mortgage Bond (Friday Dec 16, 2022)

Economic Calendar for the Week of December 19 – 23

A Look into the Markets

This week, interest rates touched the lowest levels in two months on the idea that inflation may have peaked. Let’s break down what happened and look into Thanksgiving Week.

“Well I’m going down. Down, down, down, down, down” Going Down by Jeff Back

10-yr Note Touches 3.67%

The 10-yr Note yield touched 3.67% this week, a large rate improvement from 4.23% seen the previous week. The downtick in long-term rates also fed into home loan rates, which have declined as much as .50% in the last week or so.

The big question? Does this decline in rates have “legs” and will it continue?

Peak Inflation Equals Peak Rates

The readings on inflation suggest that we may have just seen the peak in inflation. We will want to see future inflation readings to confirm this, but long-term bonds, which are forward-looking, appear to be pricing at a peak.

Do not tell the Federal Reserve that inflation may have peaked. There were several Fed speakers out this week saying that inflation is still a problem, and they want to keep rates higher for longer.

Short-Term – Higher for Longer

Remember, when the Federal Reserve says they want rates higher for longer, they are talking about the Federal Funds Rate, which is an overnight rate that banks lend to each other. The Federal Funds Rate affects short term loans like credit cards autos and home equity lines of credit.

It is important to note that while the Fed Funds rate may increase by another 1.25% between now and next May, long-term rates like the 10-yr Note and mortgages, may have already peaked.

Smaller December Hike

The financial markets are now pricing in a high probability the Federal Reserve will only raise rates by .50% next month. Additionally, the markets are also sensing the Terminal Rate, or peak in the Fed Funds Rate will be 5 to 5.25% achieved by May of 2023. The Fed will attempt to lift rates that high and keep them there if the economic readings will support it.

Should we see the labor market struggle and inflation come down even further, the Fed may be forced to do less hikes. As the old saying goes, time will tell.

Bottom line: Home loan rates have improved. With more inventory coming to market and many sellers eager to make deals, now could be a great time to consider taking advantage of the opportunities in housing.

Looking Ahead

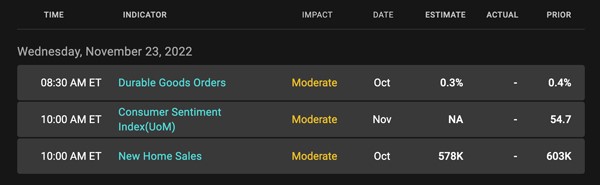

Next week we celebrate Thanksgiving, which means bonds are closed Thursday and only open a half day on Friday. There is also little in the way of economic data, with just Durable Goods Orders and Consumer Sentiment on Wednesday. There will be plenty of Fed speakers out to remind us of the need to hike rates more.

Mortgage Market Guide Candlestick Chart

Mortgage-backed security (MBS) prices determine home loan rates. The chart below is a one-year view of the Fannie Mae 30-year 5.5% coupon, where currently closed loans are being packaged. As prices go higher, rates move lower and vice versa.

You can see on the right side of the chart the Green Candles moving higher means a nice improvement in rates. For rates to improve further, we need to see MBS climb above $101, which will serve as a ceiling of resistance.

Economic Calendar for the Week of November 21 – 25