A Look into the Markets

This week home loan rates improved modestly as we approach an important Fed Meeting and inflation reading next week. Let’s discuss what happened and talk about the headline risk on the horizon.

“I’m just waiting on a Friend” – Waiting on a Friend by The Rolling Stones.

More Signs Of Inflation Falling

On Tuesday, 3rd Quarter Productivity showed that Unit Labor Costs (how much a business pays its workers to produce one unit of output), came in lower than expectations. If it costs less to produce something, there is no pressure to charge more, thereby lowering inflation expectations.

The Productivity and Unit Labor Costs reading do not typically move the market that much, but in a world looking for signs that inflation is abating, this soft reading pushed bond yields sharply lower.

3.40%

Back on Nov 8th, the 10-yr Note yield peaked at 4.20%. One month later, yields fell all the way down to 3.40%, matching the lowest level since mid-September.

Mortgage-backed securities (MBS), which is where home loan rates are derived, moved more sideways and didn’t experience the large rate improvements seen in Treasuries. That is OK as mortgage rates also remain at the lowest levels since September.

2/10 Yield Curve Inversion

The yield on the 10-yr Note dropped over .80% beneath the 2-yr Note for the first time in over 40 years. Why is this important to us? Nearly every time the 2-yr yield moves above the 10-yr yield, a recession soon follows. Seeing the inversion steepen to levels last seen when Reagan was President suggests the threat of a recession is elevated. So, it seems, the financial markets have moved on from the threat of inflation to the threat of a recession.

Policy Error

Here’s a term that is starting to catch the airwaves. Essentially it means the Fed will raise rates too high or try to keep them high for too long and push the economy into a recession. Remember, long-term rates only move higher with the Fed Funds Rate (the rate the Fed hikes) IF the economy can absorb those hikes. The bond market is clearly challenging the idea of a “higher for longer” Fed Funds Rate with the 10-yr Note falling as fast as it has over the past month.

Bottom line: Rates have improved and sellers are eager to make deals. This may pose great opportunities for a nimble buyer. This is not an environment to wait until everyone hears about the improvement in rates.

Looking Ahead

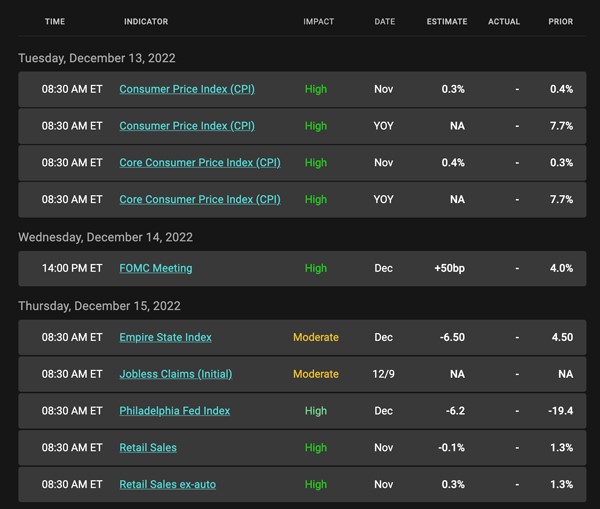

Next week is filled with headline risk. On Tuesday, the Consumer Price Index, will be reported and this reading on consumer inflation could be a big market mover. But the main event is the Fed’s Monetary Policy Decision. It is widely expected they raise the Fed Funds Rate by .50%. What will have the market’s attention is any words about a smaller hike going forward in response to “policy lags”, where we wait for existing rate hikes to impact the economy.

Mortgage Market Guide Candlestick Chart

Mortgage-backed security (MBS) prices determine home loan rates. The chart below is a one-year view of the Fannie Mae 30-year 5.5% coupon, where currently closed loans are being packaged. As prices go higher, rates move lower and vice versa.

You can see on the right side of the chart the Green Candles moving above $101 for the first time since September. Next week’s big events may determine if prices break above $102 and move a leg lower still.

Chart: Fannie Mae Mortgage Bond (Friday Dec 9, 2022)

Economic Calendar for the Week of December 12 – 16

A Look into the Markets

This week, interest rates touched the lowest levels in two months on the idea that inflation may have peaked. Let’s break down what happened and look into Thanksgiving Week.

“Well I’m going down. Down, down, down, down, down” Going Down by Jeff Back

10-yr Note Touches 3.67%

The 10-yr Note yield touched 3.67% this week, a large rate improvement from 4.23% seen the previous week. The downtick in long-term rates also fed into home loan rates, which have declined as much as .50% in the last week or so.

The big question? Does this decline in rates have “legs” and will it continue?

Peak Inflation Equals Peak Rates

The readings on inflation suggest that we may have just seen the peak in inflation. We will want to see future inflation readings to confirm this, but long-term bonds, which are forward-looking, appear to be pricing at a peak.

Do not tell the Federal Reserve that inflation may have peaked. There were several Fed speakers out this week saying that inflation is still a problem, and they want to keep rates higher for longer.

Short-Term – Higher for Longer

Remember, when the Federal Reserve says they want rates higher for longer, they are talking about the Federal Funds Rate, which is an overnight rate that banks lend to each other. The Federal Funds Rate affects short term loans like credit cards autos and home equity lines of credit.

It is important to note that while the Fed Funds rate may increase by another 1.25% between now and next May, long-term rates like the 10-yr Note and mortgages, may have already peaked.

Smaller December Hike

The financial markets are now pricing in a high probability the Federal Reserve will only raise rates by .50% next month. Additionally, the markets are also sensing the Terminal Rate, or peak in the Fed Funds Rate will be 5 to 5.25% achieved by May of 2023. The Fed will attempt to lift rates that high and keep them there if the economic readings will support it.

Should we see the labor market struggle and inflation come down even further, the Fed may be forced to do less hikes. As the old saying goes, time will tell.

Bottom line: Home loan rates have improved. With more inventory coming to market and many sellers eager to make deals, now could be a great time to consider taking advantage of the opportunities in housing.

Looking Ahead

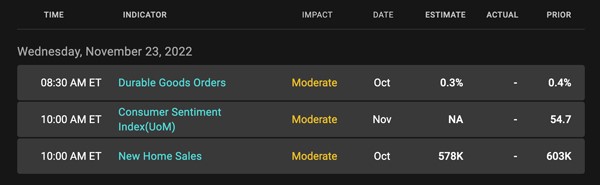

Next week we celebrate Thanksgiving, which means bonds are closed Thursday and only open a half day on Friday. There is also little in the way of economic data, with just Durable Goods Orders and Consumer Sentiment on Wednesday. There will be plenty of Fed speakers out to remind us of the need to hike rates more.

Mortgage Market Guide Candlestick Chart

Mortgage-backed security (MBS) prices determine home loan rates. The chart below is a one-year view of the Fannie Mae 30-year 5.5% coupon, where currently closed loans are being packaged. As prices go higher, rates move lower and vice versa.

You can see on the right side of the chart the Green Candles moving higher means a nice improvement in rates. For rates to improve further, we need to see MBS climb above $101, which will serve as a ceiling of resistance.

Chart: Fannie Mae Mortgage Bond (Friday Nov 18, 2022)

Economic Calendar for the Week of November 21 – 25