This past week, interest rates moved up a bit as we saw some good news getting offset by the bad. Let’s break down what went down and what’s coming up this week.

“Good times bad times I know I’ve had my share” …Good Times Bad Times by Led Zeppelin.

The Bad Times

The major headline this week was the rising conflict in the Middle East between Israel, Iran, and Lebanon. Normally, this kind of geopolitical tension would push people to invest in bonds, driving rates down due to the uncertainty.

But, when tensions rise in that region, oil prices usually follow, and that’s exactly what happened. Higher oil prices mean more inflation, which is bad news for long-term bonds like mortgages.

More Bad Times

On top of that, we’ve got strikes at major ports along the East Coast and Gulf regions. Workers are pushing back on wages and automation. If this strike drags on, it could lead to product shortages, which would drive prices up temporarily. Plus, it could slow down economic growth over the next few months—something to keep an eye on.

Some Good Times

On the brighter side, the Fed has been laser-focused on the labor market, especially now that inflation seems to be easing a bit. Last week, the job market delivered some positive surprises—more jobs were available and more private payrolls were added than expected.

But as is often the case, good news for the economy can be bad for bonds. This stronger labor market makes a quick 0.50% rate cut unlikely in the short term. On the upside, it also hints at a possible soft landing for the economy, where we manage to bring inflation down to the Fed’s 2% target without hitting a full-blown recession. Of course, this story will evolve, but for now, the good news is keeping a cap on how much rates can improve.

Fed Chair Powell Speaks

Early in the week, Fed Chair Jerome Powell spoke and reminded everyone that rate cuts are likely to be gradual. Based on what we’ve seen so far, it looks like those big 0.50% cuts aren’t in the cards anytime soon.

3.80%

For the past week, the 10-year Treasury note has been flirting with, but not quite breaking above, 3.80%. A solid close above that mark would be bad for rates in the near term. Right now, 3.80% is kind of the ceiling, but if we break through, it could quickly become the floor, meaning rates won’t improve much.

Bottom line: When the economy does well, rates suffer, and the opposite is true. If we’re going to see rates improve from here, we’ll likely need to see some softer economic data, especially since rates have already dropped a lot in anticipation of that first Fed rate cut.

Looking Ahead

Next week is packed with big events. We’ve got the Consumer Price Index (CPI), which will give us a key read on inflation. If inflation continues to moderate, that’s good news for long-term rates and gives the Fed more breathing room to focus on the labor market.

But if inflation comes in hotter than expected, things could get complicated. Also, the Treasury is selling billions of dollars in new debt, and if the market doesn’t show strong demand for that, we could see rates move higher. Finally, we’ve got the Fed minutes from the September meeting coming out on Wednesday—markets will be paying close attention to those.

Stay tuned, things could get interesting!

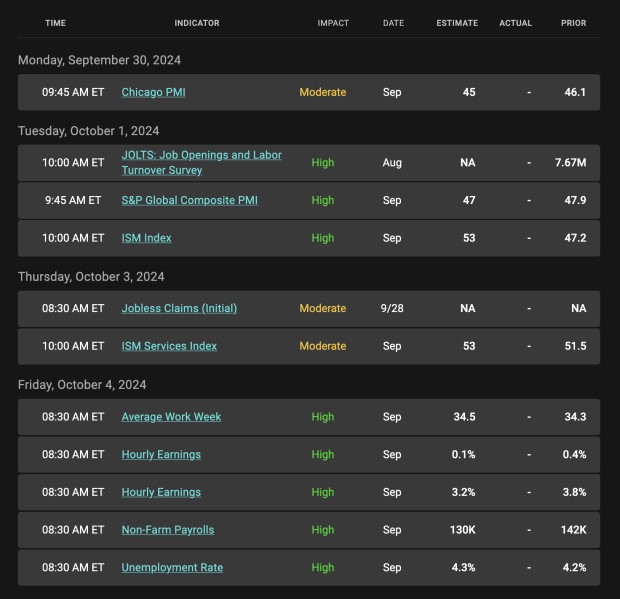

Economic Calendar

Mortgage bond prices determine home loan rates. The chart below is a one-year view of the Fannie Mae 30-year 5.0% coupon, where currently closed loans are being packaged. As prices move higher, rates decline, and vice versa.

If you look at the right side of the chart, you can see how prices and rates improved in anticipation of the Fed rate cut but have since worsened.

Chart: Fannie Mae Mortgage Bond (Friday October 4, 2024)

Economic Calendar for the Week of October 7 – 11