This past week, interest rates ticked up slightly from their lowest levels of the year. Let’s break down what happened and look at the big stuff coming up.

“Shout it, shout it, shout it out loud” – Shout it Out Loud – Kiss

Mixed Signals from the Fed

Now that the “quiet period” is over, Fed officials are back out, sharing their thoughts on the economy and where interest rates might go. Fed Governor Michelle Bowman, who dissented at the last meeting and wanted a smaller cut of 0.25%, is saying the Fed should be careful with how fast they lower rates. She’s still concerned that inflation hasn’t been fully tamed.

On the flip side, Chicago Fed President Austan Goolsbee thinks there’s room for a lot more cuts. As of now, the Fed Funds Futures are predicting rates could be 1.50% lower a year from now, but remember, this is just a projection. Everything depends on incoming data.

Big Moves in China

China’s economy is slowing down, and they’re dealing with deflation. To counter this, China’s cutting rates sharply and even buying homes to reduce the massive housing supply. It’s going to take time to see if these strategies work, but if they do, it could impact global markets, especially if China successfully stokes inflation. We already saw oil prices tick up because of some of these measures, and higher oil prices are never good for long-term rates like mortgages.

Mortgage Demand on the Rise

The Mortgage Banking Association reported a nice bump in mortgage applications last week. Both purchase and refi demand are up, which is a solid indicator of stronger days ahead. It looks like all we need is a dip in rates to see more positive numbers. With rates likely to trend lower over time, this is good news for the market.

Key Data Incoming

The next wave of economic data is crucial. If we see negative reports—like a higher unemployment rate—this will increase the chances of more and possibly deeper Fed rate cuts (think 0.50%). But if the numbers are better than expected, the Fed might pause on future cuts, which could affect mortgage rates.

Bottom Line

Rates are still on a downward trend, though it won’t be a smooth ride. Watch for fits and starts as data rolls in.

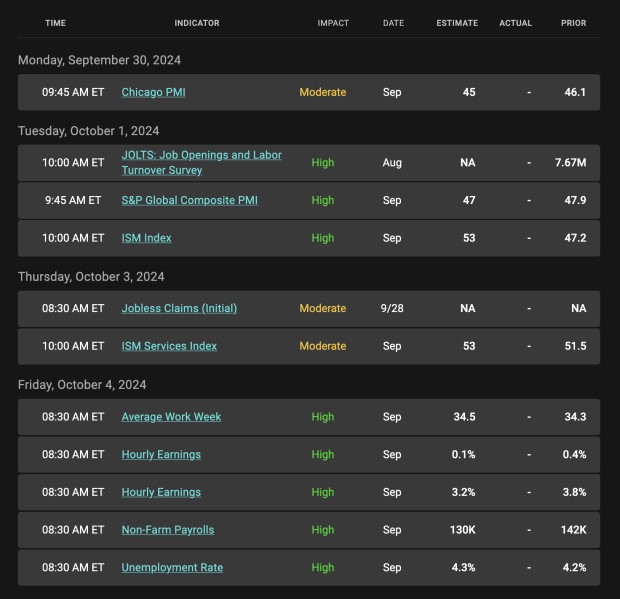

Looking Ahead

Next week is all about jobs. The Fed’s watching the labor market closely and said they don’t want to see any more “cooling.” The expectation is for 142,000 new jobs and for the unemployment rate to stay at 4.2%. If the report comes in strong, it could take pressure off future rate cuts. If not, deeper cuts might be on the horizon.

Economic Calendar

Mortgage bond prices determine home loan rates. The chart below is a one-year view of the Fannie Mae 30-year 5.0% coupon, where currently closed loans are being packaged. As prices move higher, rates decline, and vice versa. If you look at the right side of the chart, you can see how prices have backed away from the best levels of 2024 on a “buy on the rumor, sell on the news” reaction to the recent rate cut.

Chart: Fannie Mae Mortgage Bond (Friday September 27, 2024)

Economic Calendar for the Week of September 30 – October 4