This past week, interest rates stayed steady at their best levels in over a month. Let’s dive into what happened and what’s ahead.

“All good. In the hood tonight” All Good in the Hood Tonight by Jamiroquai.

Powell’s Outlook

“Pretty, pretty, pretty good.” – Larry David, Curb Your Enthusiasm

On Wednesday, Fed Chair Jerome Powell took the mic at a New York Times event to share his thoughts on the economy and what to expect from the Fed regarding rate cuts.

Here’s the headline: Powell believes the U.S. economy is in great shape, saying, “The U.S. economy is in very good shape, and there’s no reason for that not to continue… downside risks appear to be less in the labor market, growth is definitely stronger than we thought, and inflation has come in a little higher.”

Because of this strength, Powell says the Fed can afford to be cautious moving forward as they try to find the “neutral” rate—where the economy hums without overheating.

Addressing why the Fed made a hefty 0.50% rate cut in September but is taking a lighter touch now, Powell pointed to updated data: “What happened instead was in the couple of months after that, we got some data revisions, which strongly suggest the economy is even stronger than we thought.”

Of course, the story can flip again quickly. Inflation could heat up, or the labor market could weaken, and the Fed might have to pivot. But for now? Things are looking steady.

Realtor.com’s Housing Outlook

Adding to Powell’s optimism, Realtor.com shared their 2025 housing market forecast—and it’s shaping up to be a positive year for buyers and sellers alike.

Here’s the breakdown:

- Mortgage Rates: Average 6.3% for the year, easing to 6.2% by year-end.

- Home Prices: Projected to rise 3.7%, continuing the growth streak since 2012.

- Rents: Holding steady with a slight 0.1% drop.

- Inventory: Existing home inventory expected to jump 11.7%, building on 2024’s momentum.

- New Construction: Single-family home starts to climb 13.8% to 1.1 million—the highest since 2006.

- Home Sales: Predicted to increase 1.5% year-over-year, reaching 4.07 million.

- Months’ Supply: Improving from 3.7 months in 2024 to 4.1 in 2025. Under 4 months favors sellers; 4-6 months signals balance.

Key takeaway: If you’re thinking about buying, don’t wait. Rates aren’t dropping much, and prices are still on the rise.

Labor Market Holds Strong

Earlier this week, the JOLTS report surprised markets with a bump in job openings and an uptick in workers voluntarily quitting their jobs (the “Quits” indicator). When people quit, it’s often because they’re confident they can find something better, and this metric is back to pre-pandemic levels—a sign of a resilient labor market.

Also in the mix was a significant drop in Continued Claims (those receiving unemployment benefits for more than a week), another labor market bright spot.

With jobs being the foundation for home buying and the Fed watching the labor market closely, these readings were welcome news.

Bottom Line

Interest rates are stabilizing after a turbulent selloff since September. However, with the new Administration and fiscal policy changes still a couple of months out, brace for continued market swings and potential rate volatility.

Looking Ahead

Next week kicks off the Fed’s Blackout Period, meaning no speeches or statements from Fed officials to shake up the markets. But keep an eye on the Consumer Price Index—a key inflation reading. It’s running at 3.3% annually, higher than the Fed prefers. A hotter reading could push rates up, while a cooler number might offer some relief.

Stay tuned!

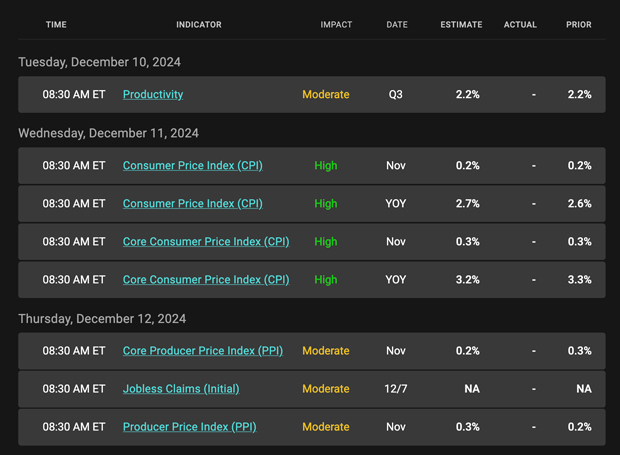

Economic Calendar

Mortgage bond prices determine home loan rates. The chart below is a one-year view of the Fannie Mae 30-year 5.5% coupon, where currently closed loans are being packaged. As prices move higher, rates decline, and vice versa.

If you look at the right side of the chart, you can see how prices have jumped higher and are testing $100. Much like how Bitcoin is attempting to make $100,000 a floor. If Mortgage Bonds can close above $100 and make it a floor, current rates will go from being about as good as they could get to about as bad as they can get.

Chart: Fannie Mae Mortgage Bond (Friday December 6, 2024

Economic Calendar for the Week of December 9-13