This Week in Rates: They’re Still Climbing 🚀

As We Get Closer to Election Day…

Interest rates kept doing what they’ve been doing lately—heading up. So, let’s dig into what’s been going on with the economy and how it might play into what we see at the polls and from the Fed.

“Now I’m walking on sunshine, whoa-oh, I’m walking on sunshine, whoa-oh I’m walking on sunshine, whoa-oh And don’t it feel good” Walking on Sunshine by Katrina and The Waves

Recession Fears? Not So Much Anymore

On Wednesday, we got the first look at the 3rd Quarter GDP, which came in at 2.8%—a bit softer than expected, but still not bad. For the year, we’re on track for around 2.5% growth, mostly thanks to strong consumer spending. Remember when that weak August jobs report made everyone think a recession was coming? Now, with a strong September report and a surprising drop in unemployment, those recession worries are fading fast. The takeaway? The economy and labor market are holding up better than expected, and for now, that’s keeping recession fears at bay.

Inflation’s Not Going Anywhere (Yet)

Inflation, particularly the “core” stuff (excluding food and energy), keeps sticking around at higher levels. This is one reason the Fed’s future rate cuts probably won’t be as generous as last time when they did a 0.50% cut in September. And, it’s also why mortgage rates have been climbing since mid-September. Until inflation chills out, we’re likely to see rates stay elevated.

Consumers Are Feeling Good

The latest Consumer Confidence numbers jumped to 108.7, the highest we’ve seen since 2021. With Election Day approaching, people seem a bit more optimistic. Fewer folks expect a recession, and more are feeling good about buying a house, a car, or even stocks in the coming months. That’s a big vote of confidence in the economy, and it’s good news overall.

Pending Home Sales on the Rise

In September, when rates took a dip, pending home sales spiked to their best levels since March. But with rates creeping up again, October might not look as rosy. This just shows how hungry people are for housing right now, but they need lower rates to make it happen.

The 10-Year Note: All Eyes on 4.35%

The 10-year Treasury Note (the one that tends to push mortgage rates up or down) has been breaking resistance levels since mid-September. Right now, it’s sitting at 4.35%. If it breaks above that, we could see mortgage rates inching even higher.

The Bottom Line: Ever heard the saying, “The cure for higher rates is… higher rates”? When yields get high enough, it can attract buyers to bonds, which might help ease rate hikes. With Election Day and the Fed meeting next week, we’re about to see if mortgage rates might finally hit their peak.

What’s Coming Up?

Next week is huge for markets and the country as a whole. Tuesday is Election Day, with a lot on the line for the presidency and Congress. Then on Thursday, the Fed is set to release its latest policy statement. Right now, markets are betting on a 0.25% rate cut, but as always, the Fed could surprise us. Buckle up—it’s going to be an interesting week!

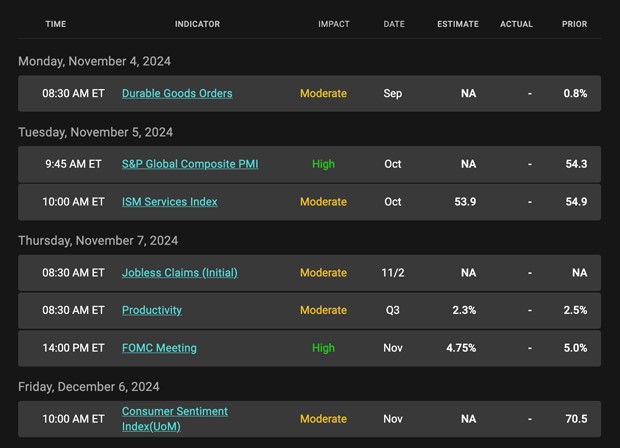

Economic Calendar

Mortgage bond prices determine home loan rates. The chart below is a one-year view of the Fannie Mae 30-year 5.0% coupon, where currently closed loans are being packaged. As prices move higher, rates decline, and vice versa.

If you look at the right side of the chart, you can see the trend of lower prices and higher rates remains intact.

Chart: Fannie Mae Mortgage Bond (Friday November 1, 2024