This past week, we’ve seen interest rates creep up as signals of “higher for longer” trends emerge globally. But before diving into the news, let’s take a moment to reflect on Memorial Day and its significance.

Originally called Decoration Day, Memorial Day was first observed after the Civil War to honor those who died in military service for our country. Declared a federal holiday in 1971, it’s commemorated on the last Monday in May. For many of us, Memorial Day weekend marks the unofficial start of summer, filled with travel, backyard barbecues, time on the water, and cherished moments with family and friends.

As Dolly Parton beautifully sings in “Color me America” “I am Red and White and Blue / These are Colors that Ring True.”

The Fed’s “Higher for Longer” Stance

Last Wednesday, we got a look at the minutes from the Fed’s meeting three weeks ago. Most Fed officials don’t see a need to cut rates anytime soon. At that meeting, Fed Chair Powell made it clear they weren’t planning to hike or cut rates. Now, with the minutes out, it’s evident the Fed is waiting for inflation to move “sustainably towards 2%” before considering cuts, unless we see signs of a weakening labor market. For now, any rate hike has been postponed until November.

The UK’s Economic Shift

Last week, the UK reported higher-than-expected inflation, pushing the possibility of a rate cut further into the year. This caused interest rates to spike globally, including here in the U.S.

Nvidia’s Strong Performance

After the bell on Wednesday, Nvidia reported earnings that far exceeded expectations. Their optimistic sales outlook, driven by advancements in AI, boosted stock prices, reinforcing the “higher for longer” sentiment in the market.

Dimon’s Warning

JP Morgan Chase CEO Jamie Dimon, speaking in Shanghai, warned of a potential “hard economic landing” in the U.S., which could bring about stagflation—slower growth paired with higher prices.

Bottom Line

For now, we’re in a “higher for longer” scenario. The Fed’s position could change with a shift in the labor market or signs of moderating inflation.

Looking Ahead

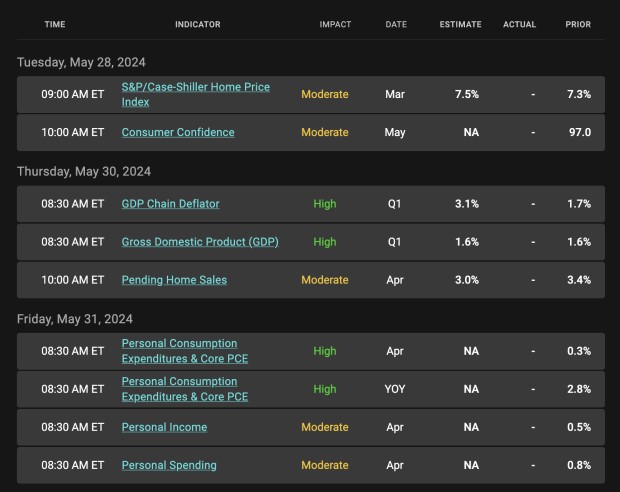

Next week, keep an eye on the Fed’s preferred inflation gauge, the Core Personal Consumption Expenditure (PCE), which they want to see move towards 2.00%. Expectations are for a reading of 2.7%, indicating there’s still work to be done to reach the Fed’s target. We’ll also get updates on GDP, Consumer Confidence, and Housing Data.

Let’s take this Memorial Day to remember and honor those who have sacrificed for our freedoms, and as we enjoy time with loved ones, let’s stay informed about the economic trends shaping our future.

Economic Calendar

Mortgage bond prices determine home loan rates. The chart below is a one-year view of the Fannie Mae 30-year 6.0% coupon, where currently closed loans are being packaged. As prices move higher, rates decline, and vice versa.

If you look at the right side of the chart, you can see how prices have backed away from the best levels in a month as the “higher for longer” narrative has gained momentum.

Chart: Fannie Mae Mortgage Bond (Friday May 24, 2024)

Economic Calendar for the Week of May 27 – 31