A Look into the Markets

The quiet before the storm. This past week, Fed officials were literally “quiet” with no speeches ahead of next week’s Fed Meeting where a .75% rate hike is widely expected. Let’s discuss what will be an important week ahead.

“And I’ve made up my mind, I ain’t wasting no more time – Here I go again” – Here I go Again by Whitesnake

Another Big Fed Rate Hike Coming

For the first time in over 40 years the Fed is expected to raise rates by at least .75% in back-to-back meetings.

This rate hike will have no direct impact on home loan rates, but it will increase short-term rates like credit cards, auto loans and home equity lines of credit. Consumers should also expect a boost to the interest rate in your savings accounts.

How will mortgage rates react? That is the unknown at the moment. Back in June, when the Fed also raised rates by .75%, the 10-yr Note yield hit 3.49%, the highest levels in years and moved sharply lower on increased recession fears. Today, the 10-yr Note stands near 3.00%. If the economy can absorb higher long-term rates, then we should expect long-term rates to move higher. Currently the 2-yr-Note yield is near 3.25% and inverted with the 10-yr, which typically portends a recession.

In a recession, long-term rates do not go higher, and the Fed doesn’t hike rates.

The Fed, who controls short-term rates, is hiking the Fed Funds Rate to slow demand, tamp down inflation, cool off the labor market and remove “froth” from the housing market.

Froth Removed

“Single-family starts are retreating on higher construction costs and interest rates, and this decline is reflected in our latest builder surveys, which show a steep drop in builder sentiment for the single-family market,” Jerry Konter, chairman of the National Association of Home Builders (NAHB).

With the US economy close or in a recession, we should expect housing to slow, and it is. The single-family home market is also slowing in the existing home arena. The June Existing Home Sales report showed the slowest sales pace since June 2020, at the start of the Covid pandemic.

The median price of a home sold in June hit $416,000, another record and an increase of 13.4%. Price gains are expected to slow in the months ahead to a more normal rate of appreciation – this is a good thing.

The Unemployment Line is Getting Longer

Initial Jobs Claims, a leading indicator of the labor market, showed that 251,000 signed up for unemployment benefits. This is a low historic number, but the numbers have been increasing each of the last several weeks – highlighting layoffs across the country.

Currently, there are still 2 jobs available for every unemployed person that wants a job, so the labor market remains strong, which is great for housing as well as ensuring any recession would be shallow.

Let’s hope the Fed stays true to their word and remains “nimble” in response to the incoming data which is showing signs of worsening.

Bottom line: Home loan rates appeared to have stabilized and more housing inventory has been coming to the market in many areas.

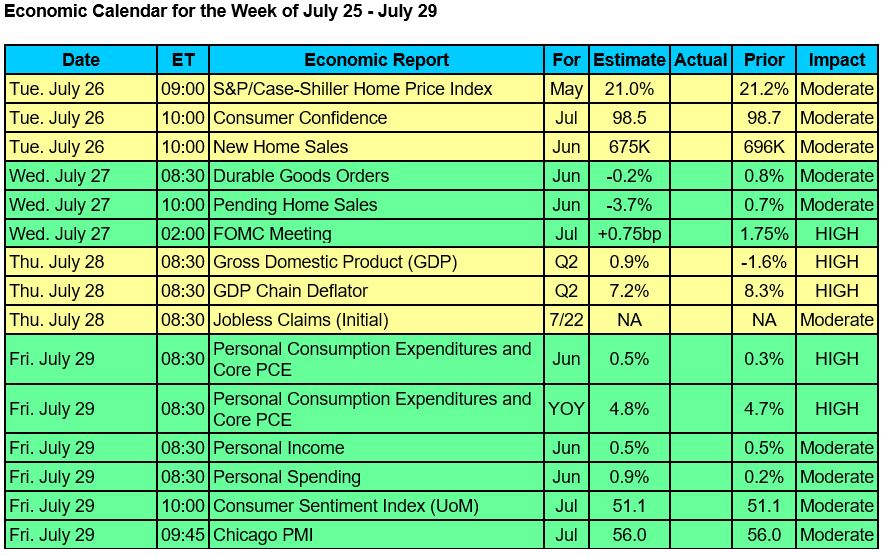

Looking Ahead

It’s Fed Week. On Wednesday at 2pm ET, the Fed will release their Monetary Policy Statement. Expect a lot of volatility. We could see multiple reactions. The first coming on the Statement, the next coming at the 2:30 pm ET Press Conference – then the more forceful and possibly different reaction next Thursday morning.

Mortgage Market Guide Candlestick Chart

Mortgage-backed security (MBS) prices are what determine home loan rates. The chart below is a one-year view of the Fannie Mae 30-year 4.5% coupon, where currently closed loans are being packaged. As prices go higher, rates move lower and vice versa.

You can see the right side of the chart; prices fell to new 2022 price lows…meaning 2022 rate highs but bounced sharply higher after the big Fed rate hike in mid-June, then gave up some of those gains in response to the recent high inflation readings. It does appear the mid-June price lows will represent the rate peaks for 2022. Next week’s Fed Meeting and action may determine whether this rate peak remains in place.

Chart: Fannie Mae 4.5% Mortgage Bond (Friday Jul 22, 2022)