As we wrap up the first half of 2024, let’s take a look at what’s been happening in the mortgage and housing markets, and what to keep an eye on in the coming week.

“I said that time may change me. But I can’t trace time” Changes by David Bowie.

Inflation Still a Big Deal Everywhere

It’s been over two and a half years since Fed Chair Powell admitted that high inflation wasn’t just “transitory.” Yet, here we are, still wrestling with it both here and abroad. Last week, Canada and Australia reported hotter-than-expected inflation. Their central banks responded by scrapping any plans for rate cuts, with Australia likely to keep hiking rates. This global inflation and higher rates put upward pressure on our own rates, causing a spike in mortgage rates this week.

Back home, Fed officials have been pretty clear about their stance on U.S. inflation. They think it’s going to stick around and possibly even rise through the end of the year. At the recent Fed meeting, they predicted inflation would bottom out this month with no significant decrease for the rest of the year. That means they don’t see interest rates dropping much, hence their forecast of just one Fed rate cut later this year.

Slowdown in Housing Sales

High mortgage rates are taking a toll on housing sales. Existing home sales are slow, even though prices are climbing nationally at a healthier pace. We’re also seeing inventory grow for the first time in a while, which could help balance things out in the long run.

New home sales are also struggling, pushing inventory to a historically high 9.3-month supply. Builders are facing challenges, too. Carl Harris, Chairman of the National Association of Home Builders, pointed out that high mortgage rates are keeping buyers on the sidelines. Builders are also dealing with higher rates for construction loans, labor shortages, and a lack of buildable lots.

Japanese Economic Woes Could Affect Us

This past week, the Japanese Yen fell to a four-decade low against the U.S. Dollar. Japan is trying to normalize its monetary policy after years of controlling interest rates. Their 10-year bond rose over one percent for the first time in 13 years.

Why should we care? Japan holds over $1 trillion in U.S. Treasury debt. There’s talk that if the Yen keeps falling, Japan might sell some of its U.S. Treasuries to buy back Yen and stabilize its value. If Japan starts selling U.S. Treasuries, it could push our rates higher.

4.35%

Despite the rise in rates, the 10-year Note yield stayed below a key resistance level of 4.35%, which helped stop the rates from spiking further. Keep an eye on this level going forward.

Bottom Line

There’s not much hope for rate relief in the near term with higher inflation threats looming. However, things can change. Fed Chair Powell mentioned that if there’s “unexpected weakness” in the labor market, they might have to change their stance on interest rates and cut them sooner and more frequently than expected.

Looking Ahead

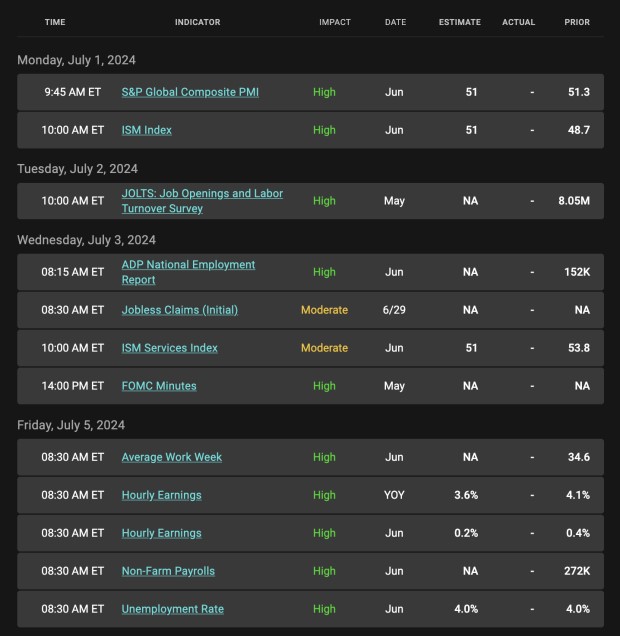

Next week is short because of Independence Day on Thursday, July 4th, but it’s packed with important economic updates. We’ll get the Minutes from the last Fed Meeting and the all-important Jobs Report. If we see surprise weakness in the labor market, the Fed might rethink their “higher for longer” rate position and cut rates sooner. Some folks on Wall Street are betting on this happening.

Looking Ahead

Mortgage bond prices determine home loan rates. The chart below shows a one-year view of the Fannie Mae 30-year 6.0% coupon, which is where currently closed loans are being packaged. When prices go up, rates go down, and vice versa.

If you look at the right side of the chart, you’ll see how prices dropped throughout the week but held steady at the end (the last green candle), as the 10-year Note yield fell from 4.35%.

Chart: Fannie Mae Mortgage Bond (Friday June 28, 2024)

Economic Calendar for the Week of July 1 – 5