A Look into the Markets

“When you believe in things That you don’t understand, Then you suffer,” Superstition by Stevie Wonder.

Producer Prices Are Falling

The Producer Price Index, which is an inflation reading on what producers/wholesalers pay for goods and services, showed a larger than expected decline. It was also the lowest reading since March 2021.

This is good news, because if producer prices fall, it leads to consumer prices falling, which leads to lower rates and less Fed rate hikes.

It appears that both inflation and long-term rates have peaked.

Weak Economic Data Elevates Recession Fears

A bunch of weaker than expected economic reports cast a dark cloud over stocks, with bonds and rates the beneficiary.

Manufacturing reports in New York and Philadelphia highlight an economic slowdown and a very weak Retail Sales number for December, showing the consumer cutting back on spending.

In the recent past, stocks had moved higher in response to weak news on the notion the end of Fed rate hikes is near. But this week, stocks slid lower on the bad news because the bad news may also mean a recession and not just the end of Fed rate hikes.

On Thursday, the 10-yr Note yield touched 3.32% for the first time since mid-September which suggests the bond market sees a slowdown and the need for the Fed to stop hiking rates.

The Standoff Continues

The Federal Reserve and the bond market disagree on the Fed’s position on rates. The Fed says it wants to keep rates higher for longer, yet the sharp decline in long-term rates and wide yield curve inversions is the bond market saying the Fed is wrong.

The good news? The markets are now pricing in a .25% Fed rate hike on February 1st. We could very well see just one more .25% rate hike in March but that will be based on the incoming data.

Bottom line: Home loan rates continue to drift lower; sellers are eager to make deals and the labor market is strong. Now is a great time to highlight the current “buyers’ market” while it exists.

Looking Ahead

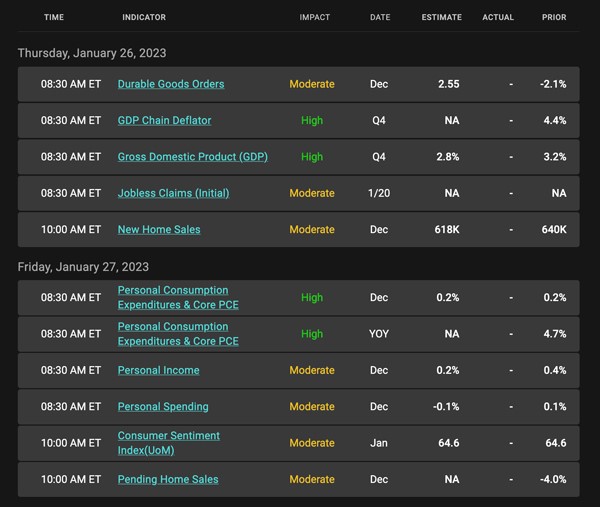

Next week is the “quiet period” for the Fed, where they do not speak or comment on monetary policy one week prior to the next Fed Meeting. But the week still carries a bunch of headline risk events, including the Fed’s favored gauge of consumer inflation, The Personal Consumption Expenditure (PCE) Index.

Mortgage Market Guide Candlestick Chart

Mortgage-backed security (MBS) prices determine home loan rates. The chart below is a one-year view of the Fannie Mae 30-year 5.5% coupon, where currently closed loans are being packaged. As prices go higher, rates move lower and vice versa.

MBS prices are right at a ceiling of resistance, which is limiting further improvement in rates. If MBS can move just slightly higher and above this nearby ceiling, rates will likely improve a bit more. The opposite is true.

Chart: Fannie Mae Mortgage Bond (Friday January 20, 2023)

Economic Calendar for the Week of January 22 – 26

A Look into the Markets

This week, interest rates touched the lowest levels in two months on the idea that inflation may have peaked. Let’s break down what happened and look into Thanksgiving Week.

“Well I’m going down. Down, down, down, down, down” Going Down by Jeff Back

10-yr Note Touches 3.67%

The 10-yr Note yield touched 3.67% this week, a large rate improvement from 4.23% seen the previous week. The downtick in long-term rates also fed into home loan rates, which have declined as much as .50% in the last week or so.

The big question? Does this decline in rates have “legs” and will it continue?

Peak Inflation Equals Peak Rates

The readings on inflation suggest that we may have just seen the peak in inflation. We will want to see future inflation readings to confirm this, but long-term bonds, which are forward-looking, appear to be pricing at a peak.

Do not tell the Federal Reserve that inflation may have peaked. There were several Fed speakers out this week saying that inflation is still a problem, and they want to keep rates higher for longer.

Short-Term – Higher for Longer

Remember, when the Federal Reserve says they want rates higher for longer, they are talking about the Federal Funds Rate, which is an overnight rate that banks lend to each other. The Federal Funds Rate affects short term loans like credit cards autos and home equity lines of credit.

It is important to note that while the Fed Funds rate may increase by another 1.25% between now and next May, long-term rates like the 10-yr Note and mortgages, may have already peaked.

Smaller December Hike

The financial markets are now pricing in a high probability the Federal Reserve will only raise rates by .50% next month. Additionally, the markets are also sensing the Terminal Rate, or peak in the Fed Funds Rate will be 5 to 5.25% achieved by May of 2023. The Fed will attempt to lift rates that high and keep them there if the economic readings will support it.

Should we see the labor market struggle and inflation come down even further, the Fed may be forced to do less hikes. As the old saying goes, time will tell.

Bottom line: Home loan rates have improved. With more inventory coming to market and many sellers eager to make deals, now could be a great time to consider taking advantage of the opportunities in housing.

Looking Ahead

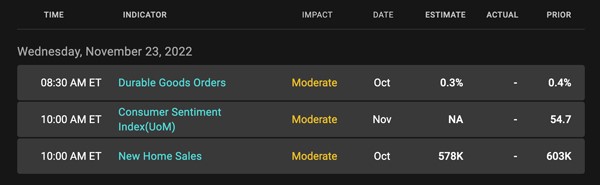

Next week we celebrate Thanksgiving, which means bonds are closed Thursday and only open a half day on Friday. There is also little in the way of economic data, with just Durable Goods Orders and Consumer Sentiment on Wednesday. There will be plenty of Fed speakers out to remind us of the need to hike rates more.

Mortgage Market Guide Candlestick Chart

Mortgage-backed security (MBS) prices determine home loan rates. The chart below is a one-year view of the Fannie Mae 30-year 5.5% coupon, where currently closed loans are being packaged. As prices go higher, rates move lower and vice versa.

You can see on the right side of the chart the Green Candles moving higher means a nice improvement in rates. For rates to improve further, we need to see MBS climb above $101, which will serve as a ceiling of resistance.

Chart: Fannie Mae Mortgage Bond (Friday Nov 18, 2022)

Economic Calendar for the Week of November 21 – 25