A Look Into the Markets

This past week, the Federal Reserve kept interest rates steady, but longer-term interest rates showed improvement. Let’s break down what happened and what we can expect in the week ahead.

“We may lose, and we may win. Though we will never be here again.” — Take it Easy, The Eagles

The FOMC Meeting

On Wednesday, the Federal Reserve released their monetary policy statement. As expected, they kept interest rates unchanged. However, their words and actions helped improve long-term interest rates, especially the 10-year Note.

Summary of Economic Projections

Every quarter, the Fed updates its Summary of Economic Projections, offering a fresh forecast on GDP, unemployment, inflation, and their “dot plot,” which indicates future interest rate trends.

-

Economic Growth: The Fed downgraded their forecast for economic growth slightly.

-

Unemployment: Their projections for unemployment have been adjusted higher.

-

Inflation: The Fed now expects Core PCE inflation to rise to around 2.8% by year-end (up from an earlier forecast of 2.5%). Despite this higher inflation forecast, they still plan to cut rates twice in 2025, with the first cut expected in June.

QT Pause

The Fed also announced that, beginning in April, they will pause their reduction of the balance sheet from treasuries. What does this mean?

In simple terms, the Fed will stop letting their treasuries roll off the balance sheet, helping to keep treasury yields from rising and bringing more stability to the market.

For us in the mortgage and housing industry, this is significant. When the Fed paused the balance sheet reduction last June, it led to improved pricing in the following months. The bond market is likely sensing this improvement, pushing bond prices higher and yields lower in response.

The Fed Press Conference

Thirty minutes after the conclusion of each Fed meeting, Fed Chair Powell holds a press conference. During this meeting, Powell was asked about the impact of tariffs on inflation. He described their effects as “transitory,” suggesting that any upward pressure from tariffs on inflation would be temporary.

The market responded calmly to this, as there is no indication that tariffs will have long-lasting inflationary effects.

Soft Data Not Enough

Powell was also asked about “soft data,” such as consumer sentiment reports, specifically the sharp increase in inflation expectations from a recent survey. While Powell acknowledged the importance of these reports, he stressed that we need to see soft data turn into “hard data” before any monetary policy changes can be made.

Oil Slides Lower

Oil briefly surged to $68 per barrel earlier this week but dropped back down to $66 following a weak outlook from Goldman Sachs. Oil prices had reached $81 a barrel in mid-January, but since then, both oil and mortgage rates have been steadily improving.

30-Year Mortgage Rate

As of March 20, 2025, the 30-year fixed mortgage rate averaged 6.67%, up slightly from the previous week when it was 6.65%.

4.20%

We are still watching the 4.20% level for the 10-year Note, which serves as a tough yield support. For long-term rates like mortgages to improve further, we’ll need to see the 10-year Note close convincingly below this level.

Bottom Line

Interest rates improved on the back of the Fed pausing QT and suggesting that any inflationary effects from tariffs will be short-lived. For rates to improve even further, we need to see bond prices push higher and break through key resistance levels.

Looking Ahead

The Fed’s favorite gauge of inflation, the Core Personal Expenditure Index, is set to be released soon. With the Fed recently raising their inflation forecast for 2025, this report will be a market mover. We’ll also see two key “soft” economic readings—Consumer Sentiment and Consumer Confidence—as well as several important housing reports on the heels of February’s improved rates.

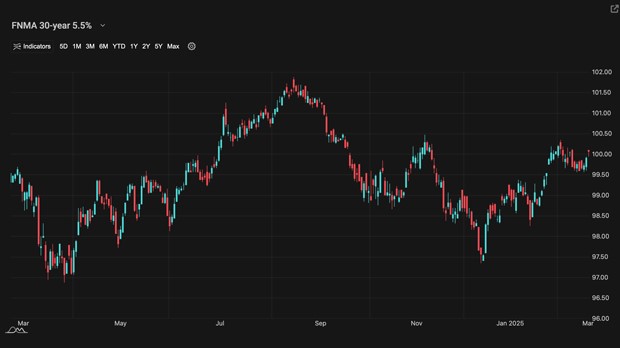

Mortgage Market Guide Candlestick Chart

For homebuyers and refinancers, mortgage rates remain a key metric, and they’re tied to mortgage bond prices. The chart below shows a one-year view of the Fannie Mae 30-year 5.5% coupon. The rule is simple: rising bond prices mean falling mortgage rates; falling prices mean rising rates. On the right side of the chart, you can see how bond prices are once again climbing toward a tough ceiling of resistance at $100.

Chart: Fannie Mae 30-Year 5.5% Coupon (Friday, March 21, 2025)